Last updated: 20 September 2025

If you have a vehicle that’s solely used for business, IRD allows you to claim the full running costs as a business expense.

But here’s the catch: Most business owners use the same vehicle for both business and personal trips. That’s where things get murky — and where a lot of people get it wrong.

Vehicle expense claims are one of the most overclaimed and audited areas in New Zealand small business tax. But they’re also one of the most underused opportunities to reduce your tax bill — legally.

In this article, I’ll walk you through:

- The 2 ways to claim vehicle expenses (and how to decide which method to use)

- 6 big mistakes that business owners make

- Answers to 7 Frequently Asked Questions (FAQs)

By the end of this article, you will:

- Understand what you can and cannot claim

- Figure out the right method for your situation

- Know what to do next if you’re still unsure

Introduction

Before I dive in, here’s the key thing to remember, and if there’s only thing you should remember from this article, its this:

Knowing the difference between 100% Business Use vs. Mixed Use.

100% Business Use: If your vehicle is only used for business purposes, you can claim the full running costs as a business expense.

Mixed Use: If your vehicle is used for both business and personal trips, you will need to work out how to allocate costs correctly (see helpful tips later in the article).

The 2 Ways to Claim Vehicle Expenses

In New Zealand, there are two main ways:

1. Kilometre (KM) Rate Method

This method involves using a set rate per kilometre to calculate the claim. This rate represents the average cost of operating a vehicle, covering fixed and running costs. If you use the kilometre rate method, you cannot separately claim additional expenses like fuel, WOF, maintenance, insurance or depreciation. The kilometre rates are published each May for the prior tax year ending 31 March.

The rates differ by vehicle type.

- Tier One Rate: First 14,000 km (both business and personal). Covers both fixed and running costs.

- Tier Two Rate: Beyond 14,000 km. Covers running costs only.

Always use the IRD’s latest rate table for the year you’re claiming.

2. Actual Cost Method

This method allows you to claim the actual expenses incurred in running your vehicle for business purposes. This includes costs such as fuel, maintenance, insurance, registration, and depreciation*. To use this method, you must keep detailed records of all expenses and the proportion of business use. This method also allows you to claim GST on the expenses if you are registered for GST.

What is depreciation? Assets such as vehicles lose value over time as they get older. This loss of value is called depreciation. Businesses claim depreciation loss as a deduction expense each tax year.

Need Help Choosing The Right Method?

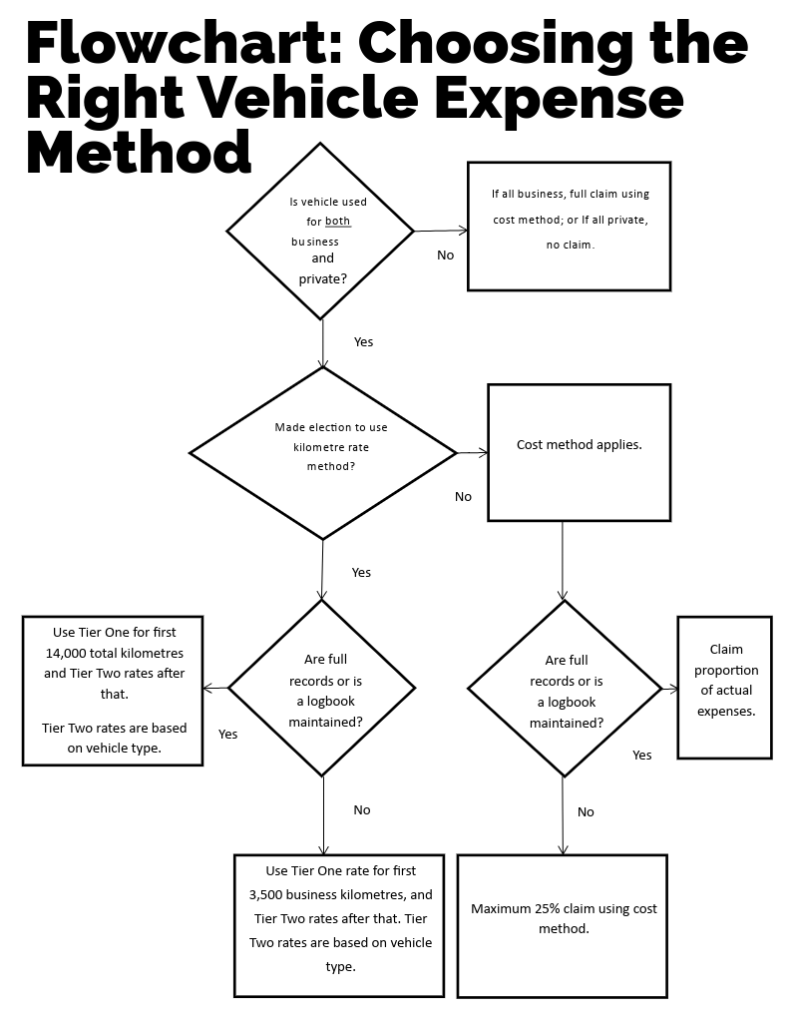

You can choose the method that best suits your circumstances, but once a method is chosen for a particular vehicle, it must be consistently applied.

Here’s a flowchart that shows whether you should use the Kilometre Rate Method or the Actual Cost Method — and what records you need to keep. If no explicit choice is made, IRD assumes you’re using Actual Costs Method by default.

Source: Inland Revenue OS 19/04

6 Common Mistakes Business Owners Make

There are 6 big mistakes that I often see business owners make:

Mistake 1. Thinking You Can Claim the Full Car Cost in Year 1

Vehicles are assets. You can’t fully deduct the purchase price upfront, though you may claim GST on the purchase if registered and eligible. The purchase cost is deducted over time via depreciation rather than immediately. Update (2025): A new temporary ‘Investment Boost’ allows businesses to deduct 20% of a new vehicle’s cost upfront (for vehicles bought on/after 22 May 2025). The remaining 80% is still claimed via depreciation. This means you get a bit more deduction in year one – but you generally cannot deduct 100% of a vehicle’s purchase price in the first year.”

Mistake 2. Treating Home-to-Work Travel as Business Use

Travelling from home to work is considered a personal trip, not a business expense — not deductible, even if the car is owned by your company or if you are self-employed. This is a general rule and exceptions are very limited.

- Can you still use a business car to travel to work?

Yes — but commuting costs remain private.

Here are three example scenarios:

- Home → Office = Private trip (non-deductible)

- Office → Client meeting → Office = Business trip (deductible)

- Office → Home = Private trip (non-deductible)

Mistake 3. Claiming Without a Logbook

Without a valid 90-day logbook, IRD generally caps your claim at 25% of running costs. Without a valid 90-day logbook, IRD generally caps your claim at 25% of total vehicle running costs. In fact, 25% is the maximum – you may be required to prove your business use even for that amount. And if you have no logbook, you cannot claim any GST on those expenses either. In short, keeping a logbook is highly recommended to substantiate your claim (for both income tax and GST purposes).

Mistake 4. Using Mixed-Use Vehicles Without Apportionment

If you use your vehicle for both business and personal trips, you will need to work out how to allocate costs correctly. This is called apportionment, and needs to be done accurately.

Mistake 5. Parking a Business Car at Home Without Restrictions

If a company car is parked at home overnight without clear restriction, the Fringe Benefit Tax (FBT) could be as high as 63.93%.

If a company vehicle is parked at home, it’s deemed available for private use (even if its not actually used for private purposes) — which triggers Fringe Benefit Tax (FBT) unless clearly restricted. Merely parking at home is enough to trigger FBT unless strict conditions are met for an exemption.

The fix?

To avoid FBT, one way is for the vehicle needs to qualify as a ‘work-related vehicle’ (e.g. permanently sign-written, not mainly a passenger car) and have a documented prohibition on personal use. If those conditions aren’t met, FBT will apply whenever the car is available for private use.

What is Fringe Benefit Tax (FBT)? This applies when non-cash benefits, like private use of a business vehicle, are provided to employees or shareholder-employees.

Does it apply to sole traders? FBT does not apply to sole traders. Sole traders are not considered employees for FBT purposes, and the vehicles they use for business are not provided as fringe benefits. Instead, sole traders must make income tax and GST adjustments for any private use of their business vehicles.

Mistake 6. No Records for Sole Business-Use Claims

Even if a vehicle is 100% business use, IRD expects evidence — a logbook, written policy, or proof of another private-use vehicle.

7 Frequently Asked Questions (FAQs)

Question 1. How Do I Determine Business Use Proportion?

Answer: IRD’s preferred method is to maintain a 90-day logbook to show the split between business and private use (Download and use Excel logbook template from the end of this article).

Alternatives could include the use of separate vehicles, actual trip records, reasonable estimates, or Commissioner’s mileage rates. But without good evidence, claims are typically capped at 25%.

Question 2. What should I do if I have not maintained a logbook?

Answer: If you haven’t kept a logbook, you should try reconstructing records (like invoices or appointment logs) to estimate business use. If that’s not feasible, you can use the Commissioner’s mileage rates or, as a fallback, claim up to 25% of running costs.

Going forward, it’s best to complete a 90-day logbook to properly substantiate business use for up to three years. Even without a logbook, make a good-faith estimate using any available data.

Question 3. What If I Have Two Cars — One for Business, One for Private?

Answer: You can claim full business costs if you can show no private use. But: Parking at home without restrictions risks FBT for company vehicles.

Question 4. What Happens If I Sell or Replace the Vehicle?

Answer: If you sell or replace your vehicle, you must record the sale proceeds, account for any depreciation recovery and GST adjustments, and start fresh with a new method and a new 90-day logbook for the replacement vehicle.

Question 5. Who Should Own the Vehicle — Me or the Company?

Answer: Company ownership can trigger FBT. Many small businesses prefer personal ownership + mileage claims to avoid FBT. Close companies can elect kilometre rate use to avoid FBT — including incorporating financing interest costs in mileage rates.

Basically, If the company owns the car and it’s available for private use, FBT is generally mandatory, so often it’s simpler to just keep it in your own name, especially if you’re a small business.

Question 6. But Are Logbooks REALLY Necessary?

Answer: Its highly recommended and IRD’s preferred method of tracking. I understand though — logbooks are a pain to maintain.

Here’s a plan you can follow:

- Do a one-time 90-day logbook: It’s valid for 3 years unless your usage changes.

- Use a GPS app that automates tracking in the background. Or rebuild travel history using Google Maps or your calendar — not perfect, but better than guessing. You can also use apps, calendar records, or other supporting docs if a daily log isn’t practical.

- Document your business travel patterns (e.g. “Every Friday I inspect rentals”).

- Keep fuel receipts and service records to match your claims.

- Record your vehicle odometer reading every year on 31 March

Even one 90-day logbook helps, provided that business usage doesn’t change significantly (by more than 20%). This logbook will help establish the business-use percentage for both the actual cost and mileage rate methods.

Question 7. What if I use my own vehicle?

Answer: If you use your own vehicle for business, you can claim all running costs if it’s strictly for business — otherwise, you’ll need to split costs between business and personal use, based on a 90-day logbook (good for 3 years). Without a logbook, you’re usually limited to claiming 25% unless you have other records to back up a higher business use.

If you’re a shareholder-employee, make sure the company reimburses you properly using IRD mileage rates or track actual costs with evidence — it’s simple once set up but messy if you wing it!

Key Takeaways

When it comes to claiming vehicle expenses, there’s no one-size-fits-all answer.

For our clients, we carefully compare both the kilometre rate and actual cost methods, and then recommend the best approach based on your vehicle use, business structure, and long-term goals.

We make sure you’re claiming everything you’re entitled to — without crossing the line into IRD trouble.

If you want tailored advice and clear answers — not guesswork — I’d love to help.

– Baqir Hussain, FCCA

Director, Finex Chartered Certified Accountants

Check Out More Free Resources

- Sign up for my weekly ‘Tax Made Simple’ newsletter HERE.

- Watch my YouTube Channel for Free Tax Tips HERE.

- Get my book ‘10 Big Property Tax Mistakes That Cost Thousands, And How to Avoid Them‘ HERE. (Video series on YouTube).

Take the Next Step

- Want to work with me? It takes 3-minutes.

- Need urgent specific advice? Book a Strategic Consultation.

- Want to learn the basics of New Zealand small business tax?

Join my waitlist HERE – Small Business Tax Course for Business Owners launching soon. Email subscribers will be the first to know.