Last week, I got a call from a rental property owner who was fuming.

“I don’t get it, Baqir,” she said. “I lost money on this property. Between the mortgage, insurance, and repairs, I had to dip into my savings to keep it afloat. So why on earth is the IRD saying I owe them tax?”

She’s not alone. I hear this all the time from property investors, especially those with a new rental property or a big mortgage.

On paper, they’re running at a loss. But when the tax bill arrives, it tells a very different story.

And I get why it’s frustrating. If you’re putting money in every month just to cover your rental, it feels like you’re already losing. A tax bill on top of that seems unfair.

The answer lies in the difference between a cash-flow loss and a tax loss.

Cash Flow vs. Taxable Income

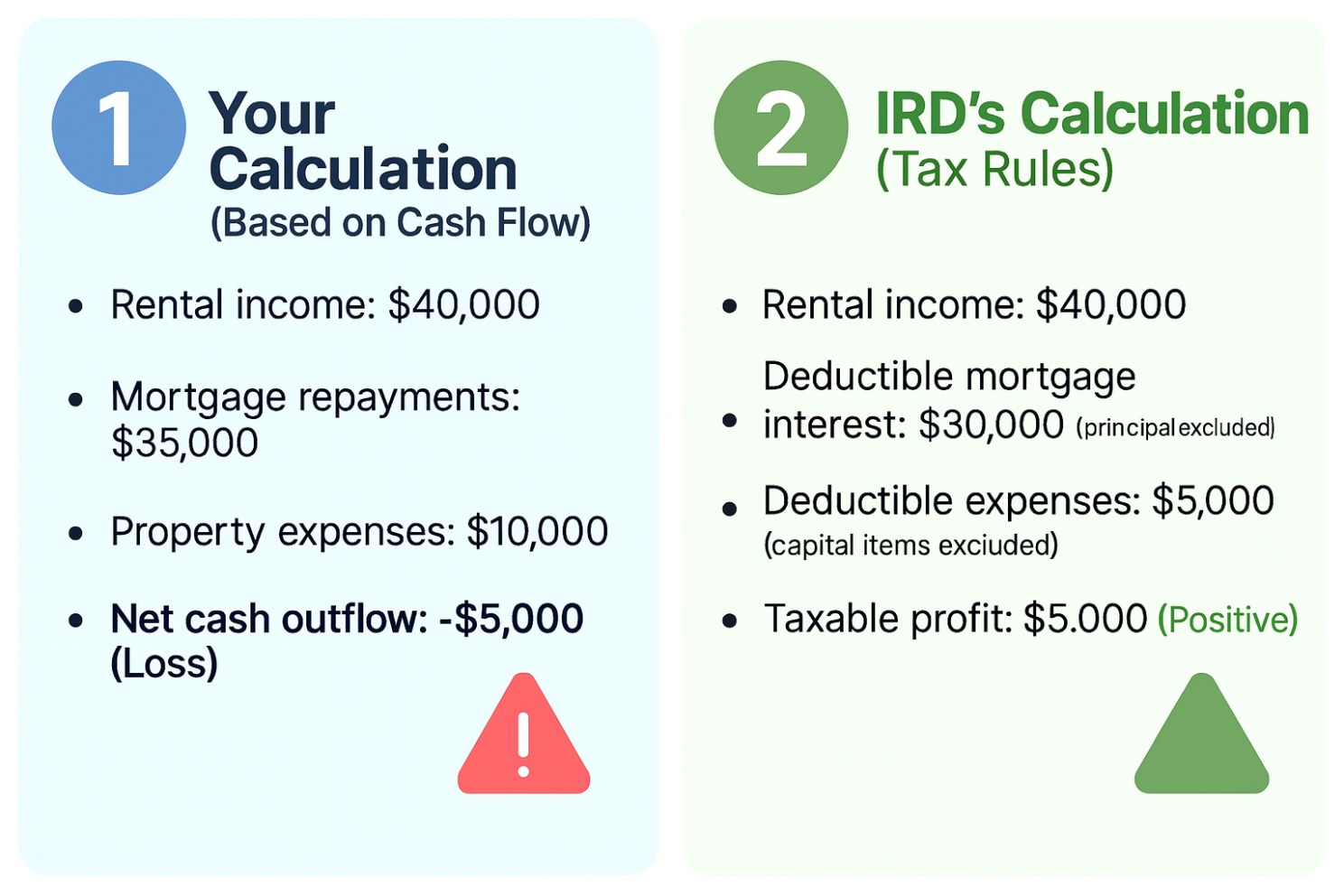

Imagine your rental property brings in $40,000 a year in rent.

- Your calculation (based on cash-flow): You expect: no tax, maybe even a refund, because you made a loss.

- IRD’s calculation (tax rules): IRD looks at the exact same numbers, and expects a tax bill, because in their books you actually made a profit.

That’s a $10,000 difference between what you expect and what IRD calculates.

Shocking, isn’t it?

Why the Numbers Don’t Match

Same rent. Same property. Same payments.

But two completely different outcomes.

Why is this?

1. Mortgage repayments: As per IRD, only the interest portion is deductible. The principal isn’t a tax expense, even though it leaves your pocket.

2. Property expenses: Not everything counts as deductible. IRD looks at the type of property expense you’ve incurred. The difference between repairs, maintenance and capital improvements is important:

- Routine repairs and maintenance are usually deductible.

- Capital improvements add to the property’s value and enhance it beyond its original state (at the time of purchase). These aren’t deductible as expenses.

So even if you’re cash‑flow negative, IRD may still assess you as having a taxable profit.

When This Hits Hard

This hits hardest for:

- New landlords who borrowed heavily, expecting a tax refund.

- Owners who made big upgrades or repairs, thinking they could claim them 100% right away.

The result? You may feel like you’re losing money both ways: out of your pocket and on your tax bill.

What This Means for You

- Don’t assume topping up the mortgage means no tax.

- Plan for tax as part of your cash‑flow forecasting.

- If you’re unsure whether a repair is deductible, get advice before you commit.

Should You Be Worried?

Yes, if you don’t understand the rules. I’ve given you two common examples of how the tax rules differ when compared to cash flow calculations.

Many property investors assume that a cash-flow loss means no tax bill, only to be blindsided later.

But IRD doesn’t work off your bank balance. It applies tax rules that often treat your “loss” as taxable income.

If you don’t factor that into your planning, it can create serious cash flow pressure. Especially if you’re topping up the mortgage from your personal income.

That’s why it’s so important to understand the basics, even if you’re not doing your own taxes. It’s not about becoming an expert. It’s about knowing enough to avoid nasty surprises.

Next Step

This article is adapted from Chapter 3 (Understanding How Property Taxes Work) of my book I published early last year.

Download your free copy below.

👉 10 Big Property Tax Mistakes That Cost Thousands (And How to Avoid Them)

About Me

I’m Baqir Hussain, FCCA, a New Zealand rental property tax specialist and author of 10 Big Property Tax Mistakes That Cost Thousands (And How to Avoid Them). I help everyday property investors legally minimise tax and avoid IRD surprises.

If you found this article helpful, feel free to share.