Ever shouted a client lunch, hosted a team party, or sent a gift hamper, and wondered how much of it you can actually claim back?

You ask yourself: “Is this 100% deductible, just 50%, or none at all?”

Most business owners get entertainment expenses wrong. That’s because entertainment is one of IRD’s most misunderstood deduction categories.

Some claim too little…

Others too much…

I want to make this simple. Here’s exactly how it works. In this guide, I’ll break down:

- How IRD defines ‘entertainment’.

- 3 main types of business entertainment expenses

- 17 examples where you can claim 100%

- Bonus: 14 more the IRD allows at 50%

- 5 common mistakes to avoid (that most business owners make)

- What you should do if you’re still unsure.

What is ‘Entertainment’ According to IRD?

IRD defines entertainment expenses as costs a businesses incurs for activities that provide enjoyment or amusement. An entertainment expense is business-related if it helps your business earn income.

Common examples of entertainment expenses include:

- Social events or staff parties

- Food and drink (meals, coffee)

- Use of pleasure boats or yachts

- Exclusive club memberships or privileges

- Corporate boxes or VIP hospitality at events

- Holiday accommodation or recreational trips

- Tickets to sporting, musical or theatrical events

- Freebies or product samples given out in business promotions

Common mistake: If the expense doesn’t help your business earn gross income, it’s considered ‘private’ and you cannot claim it as a tax deduction, even if it’s paid from your business account. In other words, “entertainment” under tax law is much broader than most people realise.

Entertainment is not just about client lunches or meals (read this): it’s almost any situation where business spending involves an element of hospitality, pleasure or socialising.

Now that you know the definition, let’s look at the 3 main types of business entertainment expenses.

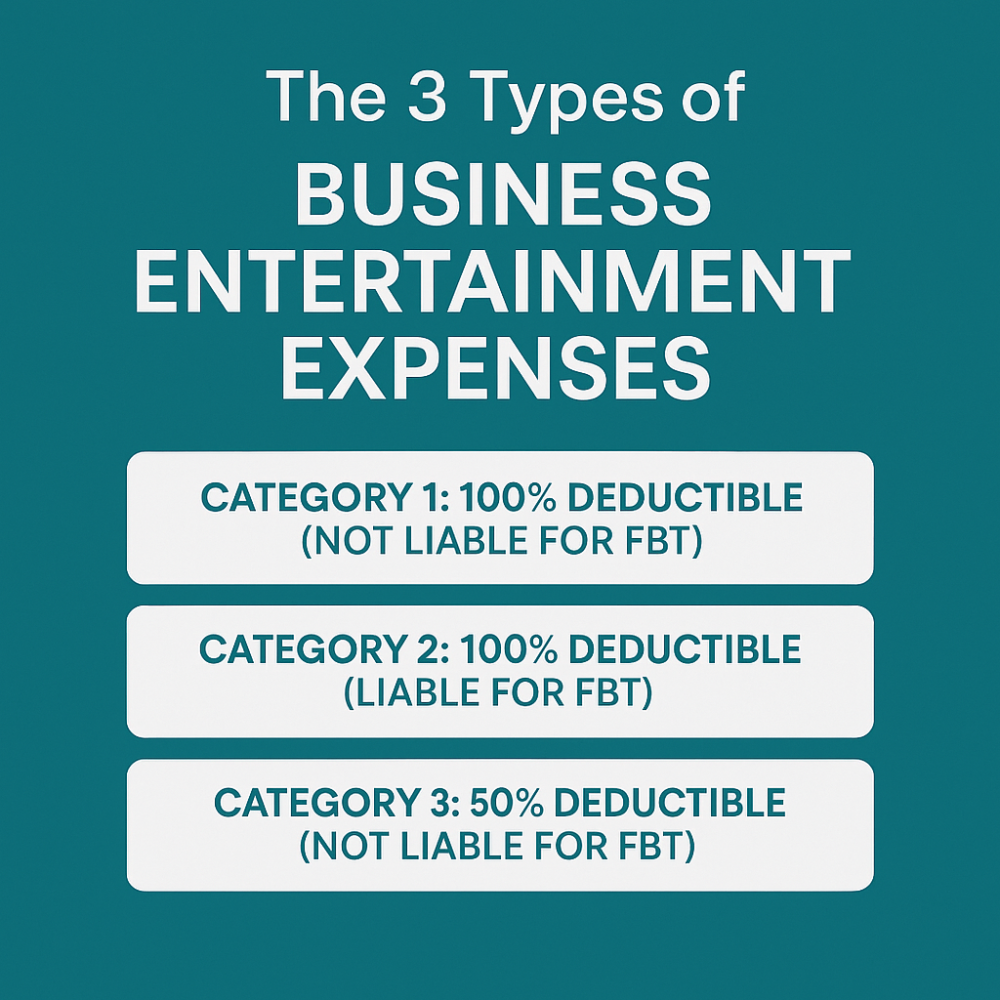

3 Main Types of Business Entertainment Expenses

There are three main types of business entertainment expenses, based on how much you can claim and whether the expense triggers Fringe Benefit Tax (short for ‘FBT’).

- 100% deductible (not liable for FBT)

- 100% deductible (liable for FBT).

- 50% deductible (not liable for FBT)

When entertainment benefits are enjoyed or received by employees, the expense may also be subject to FBT. Not all entertainment is treated the same way. The key question IRD asks is:

“Who benefits, and why?”

- If the expense has a clear business purpose (like travel meals or a public promotion), it’s usually 100% deductible.

- If it’s a staff reward or benefit, it may be subject to FBT (a tax on fringe benefits), but still fully deductible for the employer once the FBT is paid.

- If it includes a private or social benefit (even partly), IRD limits the deduction to 50%.

👉 Thinking of changing accountants?

Complete an online inquiry form to apply, I’ll personally tell you if you qualify.

17 Entertainment Expenses You Can Claim 100%

These are the entertainment costs IRD considers fully business-related (and therefore fully 100% deductible).

Some of these are subject to FBT if they benefit staff, but either way the full amount can be claimed by the business. I’ll start with the ones that have no FBT implications, then cover those that do involve FBT.

100% Deductible (and Not Liable for FBT)

1. Meals while travelling on business. Meals you or your staff buy while traveling for work are fully deductible, as they’re considered a travel cost.

Example: Dinner for yourself while attending an overnight conference in another city.

Note: If the meal is with an existing or potential business contact or it’s essentially a social event (celebration, reception, etc.), then it’s treated as entertainment and only 50% deductible. So a solo dinner on a business trip (100%), but dinner with a client (50%).

2. Food and drink at conferences or training sessions (lasting 4 hours or more). If you provide food and drink at a work-related conference, seminar or training that runs at least 4 continuous hours (excluding meal breaks), it’s fully deductible. IRD sees this as part of doing business.

Example: Lunch and coffee provided during a full-day training workshop for customers or staff. (If the event is mainly for entertainment , say, a company retreat that’s essentially a leisure trip, then the meals would only be 50% deductible)

3. Light meals for senior staff during meetings. Food or drinks provided during internal meetings, as part of normal work duties, are fully deductible. This typically refers to light refreshments for senior management or boards.

Example: Sandwiches provided during a board meeting for directors.

4. Morning or afternoon tea for employees. Everyday office refreshments like tea, coffee, biscuits and light snacks provided on your business premises are 100% deductible. IRD classifies these as minor “light refreshments” rather than entertainment.

Example: The cost of tea, coffee and biscuits for a daily morning tea in the staff room is fully claimable.

5. Business promotion open to the public. Entertainment that promotes your business and is open equally to the public is fully deductible. The key is that the public must have the same access as your employees, clients or other invitees – it’s not an exclusive event.

Example: Hosting an open-invite launch event at your store with free drinks for all attendees. Because anyone (customers or the public) can attend, it’s considered a public promotion, so 100% of those costs can be claimed.

(If the event were closed off so that the public had less access than select guests, IRD would treat it as entertainment and only allow 50%.)

6. Trade shows and expos. Food, drink or hospitality you provide as a secondary part of a trade display or expo is fully deductible. The entertainment is incidental to promoting your business.

Example: Offering free coffee or snacks at your booth during an industry trade show. Since it’s part of your promotional display, IRD lets you claim 100% of those costs.

7. Freebies and product samples. Promotional giveaways or free samples that advertise your business are fully deductible. This might include branded merchandise or sample products you hand out to customers.

Example: A tech company giving out free branded USB drives or a bakery handing out sample cookies at a market.

Note: This exclusion does not apply if the freebies are given to your employees or associates – those would fall under entertainment and only be 50% deductible.

Also, if the “freebie” is actually a gift of food or drink for someone’s personal enjoyment (like a gift basket given to a client), IRD considers that entertainment. See the 50% list later for those cases.

8. Entertainment provided for review or publicity. If you provide entertainment to someone who will review or publicize it, it’s fully deductible.

Example: A restaurant offers a free meal to a food critic or influencer for review purposes. This is essentially marketing, so it’s 100% claimable.

9. Entertainment enjoyed outside New Zealand. Entertainment costs incurred overseas for business purposes are 100% deductible. The NZ entertainment limit only applies to entertainment enjoyed within New Zealand.

Example: Taking a client to dinner while on a business trip to Sydney – that meal is fully deductible because it was outside NZ.

(Note: IRD considers the waters around NZ to be part of New Zealand for tax purposes. So, for instance, hiring a boat for a function in the Hauraki Gulf would not count as “outside NZ” and would be subject to the 50% limit.)

10. Entertainment supplied as part of your business. If your business provides entertainment as its normal trade, any costs of providing that entertainment to customers (for free or at a discount) are fully deductible. Essentially, you’re giving out your product or service as a promotion or goodwill, which is a business expense.

Example: A restaurant offering a complimentary dessert to diners, or a tour company giving a free ticket to a travel agent. Similarly, if you regularly charge for entertainment and occasionally offer it at a discount (say 50% off meals during a promotion), you can still deduct the full cost as this is part of doing business. (You’re just forgoing some revenue, which doesn’t trigger the 50% rule.)

11. Tax-free meal allowances for staff (overtime or travel). When you pay employees a meal allowance that meets IRD’s criteria to be tax-free, it’s fully deductible to your business. These allowances are considered just another staff cost.

Example: You give an employee a $30 dinner allowance because they have to work late or travel overnight for work. As long as it falls within IRD’s allowance rules (e.g. the overtime is beyond a certain length, or the travel is out of town and the amount is reasonable), the allowance is not taxed to the employee and you can claim 100% of that cost. (If an allowance doesn’t meet the tax-free criteria and you end up taxing it as part of their pay, it’s also fully deductible. See point 17.)

12. Entertainment for charitable or community purposes. Entertainment you provide for a charitable or community event that’s open to the public is fully deductible. IRD treats this like a donation or sponsorship expense rather than private entertainment.

Example: A company supplies free catering for a fundraiser at a local school or donates food to a Christmas party at a children’s hospital. Because it’s for a community/charitable purpose and not a private bash, the cost is 100% claimable.

13. Sponsorship or promotional entertainment.

If you sponsor an event or provide entertainment to promote your business, and you receive no private benefit in return, it’s fully deductible. However, if you (or your staff/clients) do receive a benefit as part of that deal – for example, you get free tickets, hospitality, or exclusive access – then you need to account for that private element by limiting that portion to 50% deductibility.

Example: Your business sponsors a local sports tournament. If all you get in return is your logo on the event banners (and maybe a shout-out), you can claim the full sponsorship cost. But if the sponsorship package includes, say, a corporate box at the finals or a VIP table at the awards dinner for you and clients, the value of that portion would be considered entertainment. In practice, you should apportion the costs – or if that’s hard, at least reduce your claim by 50% on the sponsorship to cover the private benefit element.

Key takeaway: Entertainment expenses will be 100% deductible and not liable for FBT if they are completely business related.

100% Deductible (and Liable for FBT)

The following expenses provide a personal benefit to employees, so they’re subject to FBT – but they are still fully deductible to the business once you account for that FBT. In other words, you can claim 100% of the cost, but you’ll also be paying fringe benefit tax on these items (because they’re essentially treated like additional salary in kind).

14. Restaurant or meal vouchers given as staff rewards. Giving employees vouchers or gift cards for meals, restaurants, or similar treats as a reward or thank-you is fully deductible if you account for FBT on them.

Example: You give a top salesperson a $200 restaurant voucher as a bonus. Because the employee can use that voucher on their own time (a personal benefit), IRD will require you to treat it as a fringe benefit and pay FBT on the $200. Once you do that, the full $200 cost is deductible to your business (no 50% limitation).

(Tip: Small gifts under $300 per employee per quarter are generally exempt from FBT, but if that gift is food or drink, you’re still stuck with the 50% limit on the deduction. In our example, $200 exceeds the $300 quarterly threshold when combined with other gifts, so FBT applies.)

15. Travel or accommodation prizes for employees. Rewards such as paid weekends away, travel packages, or hotel stays given to employees are 100% deductible once you pay FBT.

Example: You surprise your employee of the year with a paid weekend trip to Queenstown for them and their partner. This kind of perk clearly isn’t a necessary work expense – it’s a personal fringe benefit – so you’d declare the value and pay FBT on it. After that, the full cost of the trip is deductible to the company (no 50/50 split needed).

16. Other entertainment benefits for employees. Any other employee entertainment rewards or perks that don’t fall into wages (cash) will generally be a fringe benefit. As a rule, if it feels like you’re treating the team, and it’s not just a minor occasional thing, FBT probably applies. These are fully deductible after FBT is paid.

Example: You rent a movie theater for a private screening as a reward to staff for a big project completion. Because it’s an event solely for employees’ enjoyment outside of work duties, you could choose to treat this as a fringe benefit (especially if it’s not a one-off). You’d pay FBT on the cost, and then claim 100% of the expenses. (If such events are very occasional – e.g. your one annual party – companies often just use the 50% entertainment rule instead. But if you were doing treats like this frequently, you’d cross into FBT territory.)

17. Taxable entertainment allowances. If you give an employee an allowance or reimburse expenses for entertainment and you treat that payment as taxable income for the employee, it’s automatically 100% deductible for you. Essentially it becomes part of their salary package (you’ll deduct PAYE tax on it) and you get the full deduction, just like any wage expense.

Example: You pay a staff member a $50 per diem for meals while they attend a multi-day trade expo, and you decide to put that $50 through payroll (perhaps because it exceeds the tax-free limits or you want simplicity). The $50 will be taxed in the employee’s hands, and your business can claim the full $50 as a deduction.

(In summary: Cash paid to employees for meals or entertainment – whether as an allowance or reimbursement – is usually either tax-free to them (and fully deductible to you if it meets IRD’s rules) or taxable to them (and then fully deductible to you regardless). Either way, the 50% entertainment limit typically doesn’t apply to cash payments to staff, only to actual entertainment provided to them.)

👉 Not sure if your accountant is claiming all 17?

We regularly review this for all our clients. Complete an online inquiry form to apply. I’ll personally tell you if you qualify for ongoing tailored tax support.

Bonus: 14 More That IRD Allows At 50%

Now let’s look at the expenses that IRD considers to be part business, part pleasure. In these cases, no matter how work-related the event might feel, IRD assumes there’s a significant element of personal enjoyment – so only 50% of the cost is deductible. The 50/50 rule applies consistently, even if you think the personal element was more (or less) than 50%. In other words, you can’t argue a different split; IRD just halves it.

We’ll list the common 50% categories below. Generally, FBT does not apply to these because they’re not treated as discrete fringe benefits to particular employees – they’re more about hospitality or social situations. (There are a few fringe-benefit edge cases noted at the end.)

50% Deductible (and Not Liable for FBT)

1. Meals and drinks with clients or suppliers Any food or drink shared with clients, suppliers, or business contacts is only 50% deductible. This is the classic “business entertainment” scenario.

Example: Taking a client out to lunch, meeting a supplier for coffee, or drinks with a potential partner – you can claim half the bill as a business expense. (It doesn’t matter if you discussed business the entire time – IRD still sees an element of personal enjoyment in sharing a meal, so they only allow 50%.)

2. Staff functions, parties, or celebrations. Costs for staff social events are limited to 50% deductibility. Even though they are for employees, these are not day-to-day work duties – they’re partly social.

Example: The annual Christmas party, a Friday night drinks event, or a staff birthday lunch. Your business can claim 50% of venue hire, food, drink, entertainment etc. for those events (the other half is a non-deductible expense).

3. Team-building or morale events. If an activity for team bonding includes a recreational or social element, it falls under the 50% rule.

Example: Taking the team out for bowling, a barbecue, or paintball. These might have business benefits (morale, culture), but they’re still entertainment in IRD’s eyes – claim 50% of the costs.

4. Food and drink away from your premises (for staff). Meals or drinks you provide to employees off-site (or outside of work hours) are 50% deductible, unless they squarely meet the travel/conference exemption discussed earlier.

Example: You take your staff out to a cafe for a Friday lunch meeting. Because the meal is away from the workplace (and it’s not an overnight business trip or similar), only half the cost is claimable. (If instead you gave an employee money to buy lunch on a work trip, that would be a travel meal – different story.)

5. Food and drink on your premises (with clients/guests). If you host an event on your business premises and invite clients, customers or other guests, the food and drink provided will be 50% deductible. That’s because there’s a mix of business and hospitality going on.

Example: You hold a client presentation in your office at lunchtime and provide a catered lunch for attendees. Even though it’s at your office, because clients (non-employees) are present, IRD treats it as entertainment – claim 50%. (By contrast, if it was just your staff in that meeting eating sandwiches, that could be fully deductible)

6. Corporate boxes, marquees, or special event hospitality. Entertainment in exclusive areas at sporting or cultural events is only 50% deductible.

Example: Renting a corporate box at a Black Caps cricket match to host clients, or a hospitality tent at All Blacks rugby game, or a golf tournament. These are classic entertainment expenses – you can write off half the cost.

7. Recreational boats, yachts, or similar venues. If you use a boat or yacht (or another pleasure craft) to entertain clients or staff, only 50% of those costs are deductible.

Example: Hiring a charter boat for a client fishing trip or hosting a staff function on a yacht in the harbour. The boat hire, food and drinks on board – all fall under the 50% cap.

8. Holiday accommodation for business-related stays. Using a holiday home, lodge, or similar accommodation for business entertainment triggers the 50% limit.

Example: You take your team to a remote lodge for a planning retreat that includes leisure activities. Even if work is done, the setting is private leisure accommodation, so only half the costs are deductible. (This also applies if you let clients use your company’s holiday home – claim 50% of the expenses for that period.)

9. Recreational or social trips and outings. Any trip, tour, or outing that has a fun, social aspect (with clients or staff) will be 50% deductible.

Example: Organizing a golf or cricket day for clients, or a sightseeing tour during a conference trip. These mix business networking with leisure, so 50% is claimable.

10. Gifts that include food or drink. Business gifts are generally deductible, except when the gift is edible or drinkable. If you gift someone food, drink, or other consumable entertainment, IRD deems it an entertainment expense at 50%.

Example: Giving a gourmet hamper to a client or a referral source. You can only claim half the cost of that gift. (For non-food gifts, like a book or flowers, you can claim 100% as a marketing or staff expense. It’s the presence of food/drink that triggers the entertainment rule in gifts.)

11. Supporting costs for entertainment. Any supporting expenses related to providing entertainment that falls under the 50% category are also only 50% deductible.

Example: You hire glassware and a caterer for a client function (the function’s food and drink are 50% deductible, and so the hired equipment and staff costs are likewise 50% deductible). Another example: transportation to a social event – if you rent a bus to take staff to a party you’re throwing – that transport cost is considered part of the entertainment, so also 50%.

50% Deductible (and Liable for FBT)

Here a few situations involve employee benefits that straddle the line between the 50% entertainment rules and the FBT rules. In principle, if an entertainment benefit to staff is significant and provided as a perk, IRD will want you to treat it as a fringe benefit (so you’d pay FBT and then claim 100%). But if it’s a one-off or minor benefit, you might choose to not apply FBT, and then you’re stuck with the 50% deductibility. Here are some examples and how to handle them:

12. Employee vouchers or coupons with private use. Suppose you give an employee a voucher, ticket, or coupon that they can use on their own time for food, entertainment or leisure (for instance, a gift card to a restaurant or tickets to a show). If it’s a small gesture (under the $300/quarter de minimis threshold), you likely won’t apply FBT – but that means it’s an entertainment gift and only 50% deductible (because it’s essentially like giving them food/drink). However, if the voucher is more valuable or is a reward for their work performance, IRD will require you to pay FBT on it (since the employee can enjoy it privately whenever they choose). In that case, it shifts into the 100% deductible FBT category (as we covered in point 14 above).

Example: You give each staff member a $100 voucher for a nice restaurant as a holiday gift. You don’t exceed $300 each, so you don’t register it for FBT – but because it’s a voucher for a meal, your deduction is 50% of the cost. If you were extra generous and gave $500 vouchers, you’d have to treat those as fringe benefits (pay FBT on $500 per employee) and then you could claim the full $500 each.

13. Subsidised staff club, cafeteria or facilities. If your business funds entertainment through a staff social club, or other recreational facility for employees, the costs have a private element. Occasional use of a staff common room with coffee/tea is fine (100% deductible), but a more elaborate or regular entertainment facility gets tricky. Typically, only 50% of the cost of running such a facility is deductible. In some cases, if the benefit to each employee is significant, the subsidy might be treated as a fringe benefit – allowing a full deduction after FBT. But many businesses avoid that by keeping any subsidies low or infrequent.

Example: Your company gives $2,000 a year to the employee social club which is used to throw monthly Friday happy hours. There’s a strong social element, so you should only claim 50% ($1,000) as a deduction for those costs. (Since no individual is getting more than $300/quarter of benefit from it, you likely wouldn’t treat this as FBT – you just accept the 50% limitation.)

14. Employee entertainment offsite (not part of duties). Entertainment you provide to employees outside work premises or hours, which isn’t a necessary part of their job, is generally subject to the 50% rule.

Example: After a long day at a work conference, you take the team out for dinner and drinks at a local restaurant. This is a purely social/team activity (not a work duty), so you can only deduct 50% of that dinner bill. Such occasional staff outings are not usually treated as fringe benefits – they’re just entertainment. Only if you were doing this frequently or lavishly might IRD say “hey, this looks like a perk” and want FBT. For one-off events, stick with the 50% claim.

💬 Still confused about what’s 50% vs 100%?

Book a Strategic Consultation, and I’ll personally give you specific advice. I have a no-questions-asked, 100% refund policy if you’re not happy with the consult.

5 Common Mistakes to Avoid

The above were situations where IRD draws the line and limits deductibility. Understanding these rules helps you avoid under-claiming or over-claiming and keeps you compliant.

Even with clear IRD rules, many business owners still get entertainment expenses wrong.

Here are three of the most common mistakes I see, and how to avoid them:

- Underclaiming. Some business owners err on the side of caution and under-claim, assuming every entertainment expense must be either only 50% deductible or not deductible at all. In reality, many work-related meals are 100% claimable – for example, meals while travelling for work, meals at conferences/training, or light refreshments for staff meetings. Always check whether there’s a genuine business purpose (and no significant private benefit) before defaulting to the 50% rule. You might be leaving deductions on the table.

- Overclaiming. If you treat a 50% deductible expense as 100% deductible (when IRD says only half is allowed), or try to write off something clearly personal as a business expense, you’re overclaiming. IRD is strict about this – if there’s a personal element, generally only 50% is deductible, and if it’s entirely private (like a family outing), you can’t claim it at all. Overclaiming can result in IRD disallowing the expense later, meaning you might have to pay back the tax with interest and penalties When in doubt, check the rules or ask your accountant to avoid claiming more than you should.

- Poor recordkeeping. If you don’t keep invoices and receipts, or fail to note who was entertained and why, you’re asking for trouble. IRD expects you to have that documentation to support your claims. And if an expense has both business and private portions, be sure to record the split clearly. Without good records, you could end up losing deductions or scrambling to justify them if IRD audits you.

- Forgetting to account for FBT. If you give staff entertainment benefits such as vouchers, trips, or rewards, they may be subject to FBT. Once FBT is accounted for, the business can usually claim the full deduction. Ignoring this can create compliance issues and penalties later.

- Mixing client and staff entertainment. When you entertain both clients and staff at the same event, IRD requires you to split the costs. Only the staff portion may qualify for FBT treatment; the rest is subject to the 50% rule. Keeping these separate in your records makes your deductions easier to justify.

About Me

I’m Baqir Hussain, a Chartered Certified Accountant and founder of Finex. After 17 years in banking, audit, and regulation, including time at the Big Four and as a Principal Advisor at Chartered Accountants ANZ, I saw a big gap:

- Big businesses had easy access to world-class advice.

- Small businesses didn’t. It was too expensive, too complex, and rarely practical.

So I started Finex to change that, to make expert tax advice:

- Simple,

- Practical, and

- Accessible for everyday New Zealanders.

What to Do If You’re Still Unsure

Entertainment expenses are one of the most common areas IRD reviews, because they’re so easy to misclassify.

The rules can be confusing, but you don’t have to figure it all out alone.

It’s always better to ask questions than to guess, and potentially get it wrong.

If you’re ever uncertain about how to claim a particular expense, you have 3 options:

- Learn the rules yourself. Start with the guidance in this article.

- Talk to the IRD. They’re generally helpful and can clarify specific cases.

- Talk to your accountant. Ideally one who understands your business deeply.

💬 Need clarity on your entertainment expenses or wider tax position?

Book a Strategic Consultation to personally discuss your situation with me. I offer a 100% no-questions-asked refund guarantee if you’re not happy with the consult.

👉 Thinking longer term about switching accountants?

Complete an online inquiry form to apply, and I’ll let you know if you qualify to work with us and get ongoing tailored tax support.

(We don’t with everyone as capacity is limited , and we prefer to work with a small client base to ensure every client gets 100% quality service. Please don’t be offended if we decline your application; it’s purely to maintain our standards).