Most businesses in New Zealand are set up as either sole traders, partnerships, or companies. Each structure has its own pros, cons, and tax rules.

In this article, you’ll learn:

- The pros and cons of each structure

- How each structure is taxed; and

- The 3 simple steps to choosing a business structure that’s right for you.

Bonus

To get a personalised recommendation, download my Free Business Structure Quiz. Just answer three quick questions and get clarity in under 60 seconds.

By the end, you’ll be able to:

- Understand the key differences between sole trader, partnership, and company

- Identify which structure best suits your goals and risk profile; and

- Know what to do next if you’re still unsure

Why Choosing the Right Structure is Important

Your business structure affects three key things:

- How you’re taxed

- How much risk you carry; and

- How easy it is to grow or sell your business down the track.

Changing your structure later can be costly and, in some cases, may trigger IRD scrutiny for tax avoidance, especially if there’s no commercial reason. It’s better to get it right from the start.

The Pros and Cons of Each Business Structure

1. Sole Trader

Sole traders are people who are starting in business or are contracting. Many small business owners, contractors and self-employed people begin as sole traders. It’s the cheapest and easiest option, and may appeal to you if you want to make a living by following your passion, or to work as a contractor. The business is part of your personal finances and you’re responsible for all income and losses.

Pros of Sole Trader Structure

- Simple and cost effective to set-up, run and close.

- Low compliance costs

- No legal or registration fees

- You control the business and keep all profits.

- Losses can generally be offset against other income.

Cons of Sole Trader Structure

- More difficult to sell the business

- Harder to secure loans or investment

- May need to restructure later if you want to grow

- Requires IRD approval to employ your spouse, de-facto partner or civil union partner

- Unlimited liability: you are personally liable for business debts. Consider professional advice on protecting assets (e.g. getting professional indemnity insurance, placing assets in a trust, or considering a company structure)

2. Partnership

The Basics

A partnership is formed when two or more people or organisations come together and agree on how to share profits, debts, and duties. A partnership agreement outlines how this will work.

Pros of a Partnership

- Shared workload and decision-making

- Lower compliance and reporting than companies

- Some losses can be offset against personal income

- Easier to close than a company (in most cases)

Cons of a Partnership

- Disagreements can disrupt the business without a strong agreement

- Each partner is personally liable for debts, even those incurred by another partner.

- May need similar asset protection as sole traders (e.g. insurance, trusts or company structure)

- If a partner leaves or a new one joins, you must apply for a new IRD number

- Requires IRD approval to employ your spouse, de-facto partner or civil union partner

- ACC levies are based on each partner’s activity, so costs may differ by role.

3. Company

The Basics

A company is a separate legal entity from its owners (shareholders), managed by directors. It offers limited liability, which helps protect personal assets. Shareholders are only responsible for debts up to the value of their shares and may receive dividends.

Pros of Company Structure

- Easier to sell or bring in investors through share transfers

- Company can continue operating even with ownership changes

- Generally easier to attract funding or investment

- No IRD approval needed to employ your spouse or partner

- Enhance credibility with clients, lenders and investors

- Limited liability unless personal guarantees or reckless director actions apply

Cons of Company Structure

- More tax compliance than sole traders.

- Additional legal obligations under the Companies Act must be met.

- ACC levies are based on company activity, not individual roles. Contact ACC if your roles differ to ensure fair and cost-effective cover.

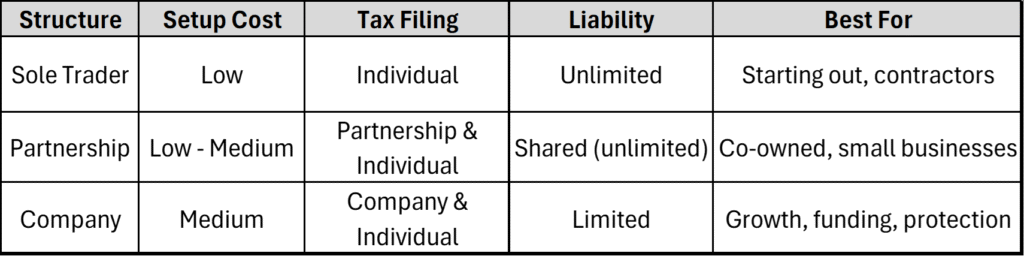

At-a-Glance Comparison Table

How Each Structure is Taxed

Lets briefly look at how income taxes work under each structure.

How is a Sole Trader Taxed?

As a sole trader, you pay tax on all income you earn from your work. You can claim work-related expenses to reduce your taxable income. You’re also responsible for ACC levies and any tax debts. Each year, you’ll need to file an individual tax return (IR3) with Inland Revenue. You will be taxed at your marginal tax rate.

(If you’d like to learn more about the basics of the NZ tax system in under 5 minutes, click here to watch my video)

How is Partnership Taxed?

At the end of each financial year, the partnership submits a tax return to Inland Revenue. Each partner also submits an individual tax return. The partnership itself doesn’t pay tax. Income is split among partners, and each partner pays income tax on their share.

How is a Company Taxed?

At year-end, the company must file a annual tax return (IR4) with Inland Revenue. A financial statements summary (IR10) may also be filed each year. Additionally, each shareholder must also file their individual tax returns (IR3).

Companies pay tax on profits at a flat rate of 28%. If profits are paid out as dividends, shareholders may pay further tax, but imputation credits help avoid double taxation. If the company makes a loss, it generally won’t pay tax and can carry forward losses to future years.

So… Which Structure Is Right for You?

3 Steps to Choosing a Business Structure That’s Right For You

Step 1: How many business owners will there be?

Ask yourself: Do I want to run this business alone or with others?

- If just you, consider sole trader or company

- If multiple people, consider partnership or company

Step 2: What are your long-term goals?

Ask yourself: Do I plan to grow, take on investors, or sell one day?

- If not, sole trader or partnership may work

- If yes, company is like the better fit

Step 3: What is your risk profile?

Ask yourself: Will this business involve significant cost, debt or legal risk?

- If yes, a company structure offers more protection through limited liability. Consider whether this gives you peace of mind.

Final Thoughts

If you’re just getting started, a sole trader setup might make sense. If you’re building something bigger or taking on risk, a company may be better. If you’re working with someone you trust, a partnership might suits, but always have a strong agreement in place.

Key takeaways:

- Choose your structure before you start. Don’t leave it for later

- Review your structure regularly as your business grows

- Restructuring later can be costly or trigger IRD scrutiny

- Sole trader is great for starting lean, company is best for scale or protection

- Always get advice if you’re unsure

Bonus

If you’re still not sure, then use my free tool. Download my Free Business Structure Quiz. Just answer three questions to help you choose the right structure for your situation.

If your situation is complex, book a Strategic Consultation with my team.

Baqir Hussain, FCCA

Director, Finex Chartered Certified Accountants

Free Resources

- Sign up for my weekly ‘Tax Made Simple‘ newsletter.

- YouTube Channel for Free Tax Tips.

- Get my book ‘10 Big Property Tax Mistakes That Cost Thousands, And How to Avoid Them‘ (Video series available here).

Want to Work With Me?

- Own a business? Fill out the Business Inquiry Form

- Own a rental property? Fill out the Rental Property Inquiry Form

- Need specific advice? Book a Strategic Consultation

Coming soon: Want to learn the basics of NZ small business tax? Join the waitlist for my Small Business Tax Course, launching soon. Email subscribers will be the first to know.

About Me

I’m Baqir Hussain, making tax simple for everyday New Zealanders. Share this article if you found it helpful.