New Zealand tax law offers a little-known way to simplify your obligations, by simply opting-out of the standard tax rules.

This is applicable for owners of properties that are used for both private and rental purposes (known as “mixed-use assets”), such as holiday homes.

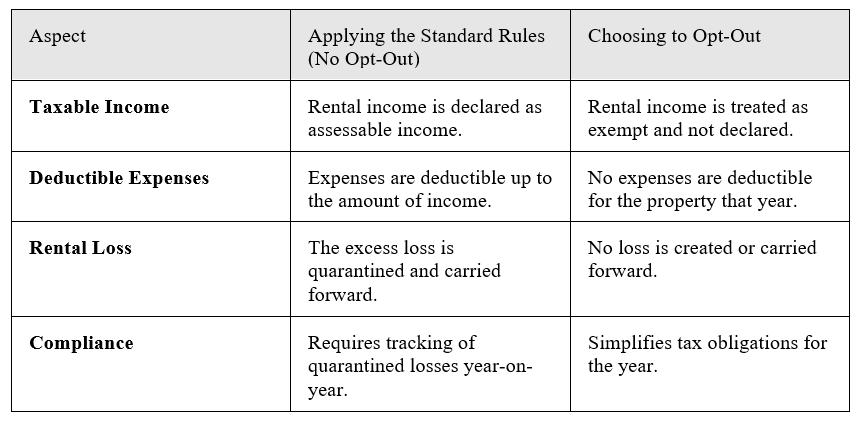

This means you pay no tax on that rental income for the year, and if you qualify, you can:

- Treat your rental income as exempt.

- Avoid reporting the income or expenses to IRD for that year.

This rule is called the Quarantined Expenditure Opt-Out.

Why Inland Revenue Allows This $0 Tax Rule

The opt-out is a simplification measure given by the IRD. It allows you to choose an easier path: instead of tracking a quarantined loss for years, you can simply remove the property’s income and expenses from your tax return for that year.

If your property’s rental income is very low compared to its value (less than 2%) and it makes a loss, the IRD “quarantines” that loss. This means you can’t deduct it against your other income. Instead, you must carry it forward to offset future profits from that specific property only.

More broadly, the tax rules for mixed-use assets are designed to prevent taxpayers from claiming significant losses on assets that are likely held more for private enjoyment than for earning income.

You need to meet two conditions to qualify.

The Quarantined Expenditure Opt-Out – Explained

You can choose to treat your rental income as exempt for the year if your rental activity results in “quarantined expenditure”. This occurs when two conditions are met:.

- Your gross rental income is less than 2% of the property’s value; and

- Your expenses for the year are greater than that income.

The resulting loss is “quarantined” and cannot be deducted against your other income. Instead of carrying this loss forward, you can choose to opt out.

The Catch: While the income becomes exempt, no deductions for any related expenses can be claimed for that year.

My Advice: To Opt-Out or Not?

The decision involves a trade-off.

Opting out offers simplicity, but carrying a quarantined loss forward may provide a greater tax benefit if you expect the property to become profitable in the future.

This opt-out offers a simple alternative to the complexity of carrying forward quarantined losses.

Key Considerations

- Mixed-Use Assets Only: These rules apply to assets used for both private and income-earning purposes that are also unused for 62 days or more in the year.

- Exclusion for Companies: The option to opt out is not available to companies.

- Annual Decision: The choice is made on a year-by-year basis for each property.

About Me:

I talk about tax, business and property, and aim to make tax simple for everyday New Zealanders.